News Flash

iGTB Pulse Newsletter January 2025

Read More News FlashEmpowering Nordic Businesses with Global Reach: A Case for CTX in Modern Treasury Management

Read More News FlashGlobal Trends Wholesale Banking for 2025

Read More News FlashTransaction Limits Management (TLM): The MRI for Corporate Payments – Precision, Clarity and Confidence

Read More News FlashElevate Your Real Estate Collections: Speed Up Your Cash Flow - Turn Days into Dollars

Learn More

Understanding Banking-as-a-Service (BaaS) and Its Value for Banks and Corporates

Home / Intellect Wholesale Banking Blog / Understanding BaaS: Value to Banks and Corporate Customers

7 Mins

Over the past few months, in literally every other client meeting I had, and all the conferences that I have attended in the post-Covid era, I have heard the terms Embedded Banking, Open Banking and Banking-as-a-Service almost consistently. It was hence a pleasant co-incidence that I was deeply involved in my firm’s go-to-market strategy on a comprehensive Banking-as-a-Service platform – I had the enviable opportunity of speaking to a wide variety of bankers, consultants, analysts and market gurus on this topic, and writing a blog on this hot topic was the natural next step!

Banking-as-a-Service is a new concept already gaining momentum, especially in the corporate banking space. It is also creating quite a stir among small and medium enterprises and leading financial institutions. Banks have realized that with the advent of digital technologies, the customer base has grown exponentially due to convenience, increased customer satisfaction, and better customer experience.

For your convenience, I have written this blog in 3 Chapters. You can access them below

For your convenience, I have written this blog in 3 Chapters. You can access them below

Chapter 3 – Coming soon

Chapter 1: Defining Banking-as-a-Service (BaaS) and Its Core Functions

1. What exactly is Banking-as-a-Service?

Banking-as-a-Service (BaaS) is the ability to embed financial products and services directly within the clients’ ecosystem as they serve their customers. BaaS provides the framework that allows banks to provide embedded finance and embedded banking products on their clients’ digital engagement platforms such as e-commerce or marketplaces.

Here’s what we will discuss in Chapter 1.

- What exactly is Banking-as-a-Service?

- Three Models of Banking-as-a-Service

- How is BaaS evolving as a concept?

2. Three Models of Banking-as-a-service –

Banking-as-a-Service, or BaaS, is a new model for customers of the bank to own the digital banking services to their end clients. In my initial market conversations, most of the use cases leaned towards a straight-forward “embedding” of banking services into a non-banking ecosystem. Still, over time, my team and I realized that the concepts were a bit broader, and we took the liberty of classifying them into 3 models, which may even potentially expand further in the future.

These three models are –

- Direct Embedding,

- White-Labeling, and

- Enabling Non-Banks

Direct Embedding

is the simplest and the most commonly used model for BaaS. In this model, the BaaS provider (the bank) embeds their banking services into the customer’s existing applications. This allows the customer to use the BaaS provider’s services without having to leave their current application.

White Labeling

is a more complex model for BaaS, with a slow yet steadily increasing rate of adoption. In this model, the BaaS provider creates a white-labelled version of their banking services that the customer can leverage. In addition to essential embedding, the customers of the bank can now become the visible face of the banking products to their end clients and own every stage of the experience from prospecting, onboarding, transaction processing, statements, account maintenance, etc. While the bank is semi-detached from the end-client / account holders, it is still involved in the process as the owner of the accounts on their books and enables full lifecycle processing.

Enabling Non-Banks

is a more recently evolving and not so frequently encountered model of BaaS, but is gaining some popularity in recent times. In this model, the BaaS provider enables non-banks to provide banking services to their end clients. These non-banks hold the accounts on their books (as opposed to the bank holding it on their books in model #2). The bank’s role here is specific to managing the transaction processing and posting lifecycle as a “banking services enabler”, despite the fact that the accounts are not held in their books

3. How Banking-as-a-Service is Evolving: Trends and Innovations

t is essential to understand that the evolution of BaaS is not an overnight trend but something that has built up over time.

In the past, banks, in addition to their own branches, enabled their products and services using their self-service channels like ATMs, online banking, mobile, wearables, etc., which they owned and managed. The evolution in technology and a more adaptive and shared ecosystem created an opportunity to “embed” banking services into any non-banking channel. This is where the whole concept of API-Banking led to a differentiated form of thinking around how services could be enabled without a lot of dependency on the bank’s own digital channel solutions. I like to think of this as a true transformative paradigm shift from traditional API banking services into a more productive ecosystem enabled through the BaaS platform offerings.

This is just the beginning since the pace of ongoing innovation in BaaS is giving rise to other possibilities and opportunities. Everyone is scrambling to innovate with more complex models that are eliminating (or diminishing) the fine lines between product offerings that are being challenged to merge and meet newer money management needs for today’s business clients.

BaaS is no longer at a “Why-do” stage of maturity and is at the “What-more-can-we-do” level currently.

Discuss recent trends and advancements in BaaS technology, including emerging BaaS platform providers and how banks adapt to changes in customer expectations and digital transformation.

Chapter 2:

I am hoping that by this time, you have read Chapter 1 where I talked about what BaaS is all about, how it evolved and the three models of how banks are offering this to their customers. If you have not read it yet, you can access it here.

So for this chapter, it only makes sense to go a little bit deeper to understand some finer dynamics of how BaaS works.

Here’s what we will discuss in Chapter 2.

- What makes Banking-as-a-Service different?

- Who’s who in BaaS?

- What is needed to enable a good BaaS solution?

1. What Makes Banking-as-a-Service Different from Traditional Banking?

Traditional Banking, as we had experienced in the past, made the bank the sole and only centre point across 3 critical dimensions of their service offerings –

- The bank owned all the technology assets like the core banking system, payment applications, etc.

- The bank also owned all the digital channel assets and solutions like online banking, mobile banking, etc.

- And lastly, the bank also owned the relationship with the customers

So consider a scenario of a non-banking firm that offers services to their customers, where they are fully online and digital but still have to rely on a bank’s digital platform to manage transactions and settlements for their customers. On the other hand, while the bank has the necessary experience and assets to enable banking services, they lack direct access to the end customers of the non-banking firm.

In simple terms, what makes BaaS different is that it enables the act of getting these parties together in an ecosystem where it is a win-win for them by creating an ecosystem of enabling (or embedding) the banking services within the digital ecosystem of the non-banking firm.

Highlight the key differences between BaaS and traditional banking, focusing on flexibility, accessibility, and customer-centricity. Discuss BaaS use cases that exemplify these differences.

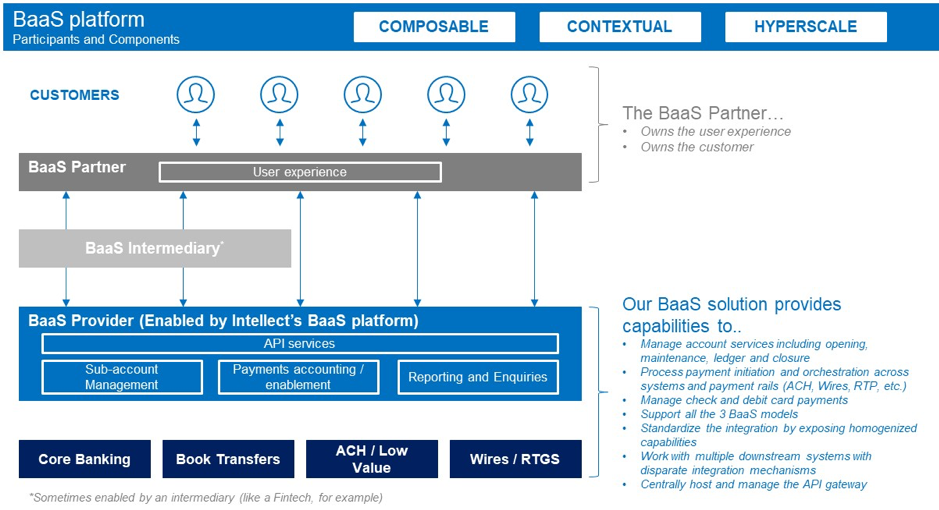

2. Who’s Who in the Banking-as-a-Service Ecosystem?

In most cases, we will typically come across two key parties that work together to enable a BaaS solution – The BaaS Provider and the BaaS Partner

THE BaaS PROVIDER – This is typically a banking license-holding institution offering various services to

- Open and close deposit accounts

- Perform KYC checks and manage regulatory compliance

- Enable balance and transaction reporting

- Process transactions via ACH or other payment rails

- Accept transactions via checks or debit cards

- Owns the technology assets like the core banking system, payment applications, etc.

THE BaaS PARTNER – Which is literally any business that would want to enable (or embed) banking services into their “non-banking” digital ecosystem, thereby providing their customers with significant ease of operations and making / receiving payments. The BaaS partner, hence

- Owns the digital channel assets and solutions like online banking, mobile banking, etc.

- Owns the relationship with the customers

With that said, the BaaS Provider is at times, unable to bring in all the technology components (we will talk about these components later in this blog) and needs some external support from a Fintech who can plug in those gaps in technology components. While not very common, we have seen banks in the market already working on these relationships to collaborate and enable an end-to-end BaaS solution. We call these Fintechs; BaaS INTERMEDIARIES.

Identify key stakeholders, including banks, fintechs, and third-party providers. Discuss their roles and contributions to the BaaS ecosystem.

3. What is Needed to Enable a Successful BaaS Solution?

A typical technology solution that addresses the key needs of the BaaS Partner and, more importantly, the end customers, requires the BaaS solution to provide a robust framework to handle the ability to –

- Create and manage the accounts for these end customers (also called virtual customers/accounts)

- Manage balances, transactions, interest (where applicable) and reporting on these accounts

- Orchestrate the money movement and report on these activities while managing exceptions

- Enable the ecosystem to manage all the APIs that can be embedded into the digital experience enabled by the service provider (your bank’s customer)

- Manage the complex end-to-end integrations between all applications

- List essential components for a robust BaaS system, including technology infrastructure, regulatory compliance, and strategic partnerships. Discuss how to select BaaS platform providers effectively.

Additionally, it is also vital for a good BaaS offering to be –

COMPOSABLE – To address the various use cases across the 3 BaaS models with a common infrastructure and not reinvent the technology every time a new business need comes up. This should also make it easy to implement a solution that can work for different market segments, again without having to reinvent the technology

CONTEXTUAL – Seamlessly blend banking into the user experience of end customers using digital systems of the BaaS Partner, and distinctly support the digital user journeys for end-customer segment and user persona

HYPERSCALE – Ensure that the platform is scalable to significant volumes, is resilient across infrastructure and application layers and designed to securely work on the open internet